The Chancellor’s 2025 Budget, delivered on 26 November 2025, introduces some of the most sweeping reforms to inheritance tax, trusts, pensions and property in over a decade.

These measures will affect anyone with a will, trust, pension, property portfolio, business interests, or long-term estate plan. Many previously reliable tax-planning strategies may no longer provide the advantages they once did, and some could now expose you to unexpected liabilities.

At Lawcomm Solicitors, we want to ensure clients understand how these changes may impact their estate and what steps can be taken to protect family wealth.

Below is a clear summary of the reforms most relevant to our clients across wills, trusts, probate, estate planning, property and business law.

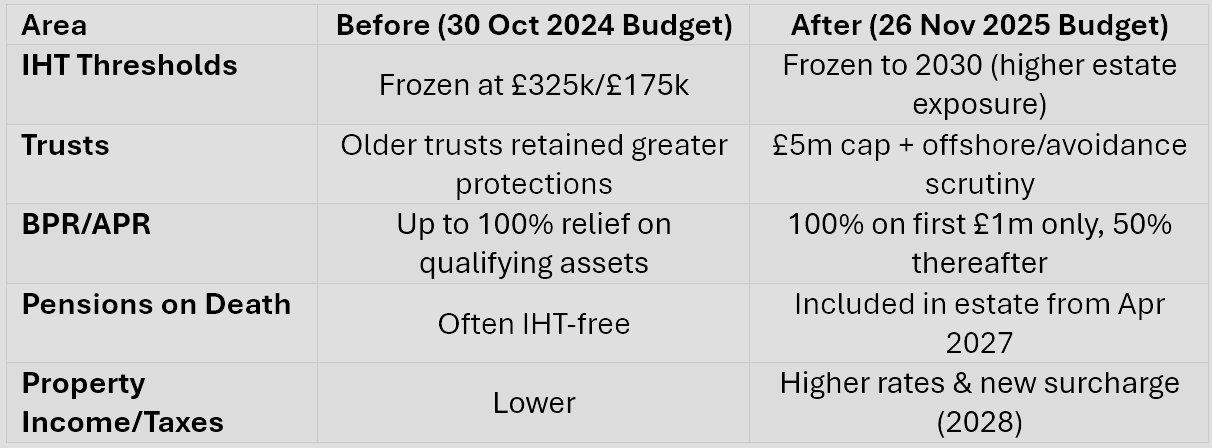

• The IHT nil-rate band (£325,000) and residence nil-rate band (£175,000) will remain frozen until 2030.

• With rising property values, more estates are likely to exceed the threshold, causing increased IHT exposure.

Even clients who previously expected to fall below the IHT threshold may now face significant tax unless planning is updated.

Trusts are a core part of estate planning, particularly for blended families, wealth preservation and IHT mitigation.

The Budget introduces:

• A £5 million cap on protections for pre-30 October 2024 “grandfathered” excluded-property trusts.

• Heightened scrutiny and anti-avoidance measures affecting trusts with offshore assets.

• Reduced tax advantages for long-standing trust structures.

A grandfathered trust is a trust created under old rules, where certain tax protections or reliefs were preserved when laws changed. Historically, older trusts, especially those holding non-UK assets enjoyed generous exclusions from inheritance tax.

The Budget now limits these protections, meaning many such trusts should be reviewed urgently.

Trusts once considered tax-efficient may no longer perform as intended; some may now create tax liabilities for trustees or beneficiaries.

Transferable £1m allowance between spouses (new concession)

As part of the Budget, the Chancellor announced a practical concession for owners of businesses and farms. From 6 April 2026, any unused £1,000,000 allowance for the 100% rate of Business Property Relief (BPR) and Agricultural Property Relief (APR) will be transferable between spouses and civil partners. This concession is drafted to apply even where the first death occurred before 6 April 2026, meaning a surviving spouse whose partner died earlier may still be able to claim the unused allowance on later death. In practical terms, where one spouse does not utilise their £1m allowance on first death, the surviving spouse may be able to benefit from an effective £2m 100% relief (the survivor’s own £1m plus the transferred unused £1m) against qualifying business or agricultural assets. This change reduces some of the immediate “farmer’s tax” impact for many families, but it does not increase the total relief available to a married couple, it simply allows unused entitlement to be preserved and used by the survivor.

From 6 April 2026:

• 100% relief applies only to the first £1 million of qualifying business or agricultural assets.

• Any value above £1 million will attract only 50% relief.

• AIM shares and certain unlisted investments may see reduced or lost relief.

Clients holding business interests, farms, or significant share portfolios may need to adjust their estate structuring to avoid substantial IHT charges.

Caveat: This concession was announced at Budget 2025 and will be implemented by statute and associated drafting. The detailed Finance Bill wording and guidance (including transitional and anti-avoidance provisions) will determine how the transfer operates in all circumstances. We recommend bespoke advice before relying on this concession in will drafting or estate restructures.

From 6 April 2027, most pension pots and death benefits will be included in an individual’s taxable estate.

Pensions have long been a cornerstone of IHT planning. Under the new rules, beneficiaries could face unexpected tax bills without careful planning and updated nominations.

Other Budget measures include:

• Higher tax on rental income, dividends and savings.

• A new high-value property surcharge due to be introduced from 2028.

• Continued restrictions on multiple-dwelling relief and interest relief for landlords.

Property and investment structures may need updating to remain tax-efficient.

We strongly recommend a review for:

• Clients with wills drafted before Nov 2025

• Anyone with existing trusts, especially older or offshore trusts

• Business owners, farmers, shareholders, and entrepreneurs

• Landlords and property investors

• Clients with significant pension funds or complex death-benefit arrangements

• Families expecting to pass on estates close to or above IHT thresholds

1. Full estate-planning review — ensure your will still achieves your goals.

2. Trust review — especially for older or excluded-property trusts.

3. Pension planning update — revise nominations before the 2027 change.

4. Business and property restructuring — model future IHT exposure.

5. Review LPAs and letter of wishes — ensure they reflect your updated structure.

6. Consider lifetime gifts or trust transfers before April 2026/2027 deadlines.

At Lawcomm Solicitors, we provide expert advice across:

• Wills and estate planning

• Trust creation, review and restructuring

• Probate and estate administration

• Lasting Powers of Attorney

• Property ownership, conveyancing and investment structuring

• Business and agricultural succession planning

• Pension-integrated estate planning

Given the scale of the 2025 reforms, a proactive approach is essential.

If you’d like to understand how the Budget affects your estate, assets, family or succession plans, we’re here to help. Contact Lawcomm Solicitors today for a confidential, no-obligation review on 01489 864 173 or email private.client@lawcomm.co.uk